Planning Your Own “Unique” Funeral — a Scary Undertaking?

{kind=link}

Renato Bialetti’s family placed his ashes in a replica coffee pot urn.

Q. I recently read about a funeral for 50-year-old Renato Garcia, where his body was on display at his own wake, wearing a Green Lantern costume. When asked why, his sister explained that she and her brother never discussed funeral wishes, but neighbors and friends suggested dressing him as the comic book superhero. Weeks earlier Garcia had found the costume in a bag of donated clothing and started wearing the guise daily. Hopefully, this is what he had wanted, but we will never know.

Now that I am getting older, I am beginning to think about my own funeral, and how I’d like to be celebrated and where I’d like to be buried. Personally, I see funerals as a way to celebrate life, and I would hate for my friends and family to wear all black, attend a religious service, and mourn over me. I would like my funeral to be a party, with my favorite music playing, and my favorite food being served. I may even want to be dressed up in my favorite red dress and have my body at the party, now that I see that that could be an option. Then, I’d want to be buried in a way that depicts how I live my life (adventurous, environmentally-conscious, fun, and free-spirited). What are some ways others have been celebrated and buried in a unique way? How do I make my wishes known to my family? I would not want them to decide for me, as was the case for Renato Garcia, the man in the Green Lantern costume. Thanks in advance for your help!

A. Funerals are meant to be some of life’s most meaningful rituals and these days are almost always framed as a celebration of the life of the deceased. They reflect the ways in which we say goodbye to those we love. Traditional funeral services work well for many people, but some want this final life event to reflect their unique individuality. Below are some examples of unique funerals and burial options:

Funerals

Doing what you love most: Some people want their bodies to be present at their funeral, in poses doing what they loved most when they were alive. These are some actual examples:

Playing poker: The dead body of Henry Rosario Martinez, a 31-year-old avid poker player from Puerto Rico, was embalmed and seated alongside his family and friends for one last game. His family organized his wake to be centered around the card game following his sudden death earlier this year.

Still doing his job: Perez Cardona, 73, a cancer patient and a veteran taxi driver honored his profession by being veiled as if he were driving his taxi.

In her favorite chair: Georgina Chervony Lloren wanted to have her funeral in her favorite rocking chair. So after she died of natural causes at age 80, her family made her last wish a reality.

Getting married: A Thai man, Chadil Deffy, married his dead fiancee after she was killed in a car accident. A ceremony was conducted at her funeral, and she was buried in a wedding gown. The couple had planned to marry, but had put off their wedding due to their busy schedules.

Riding a motorcycle: The body of biker Bill Standley was propped up on his beloved Harley Davidson motorcycle, and was displayed in a glass casket built by his two sons.

Boxing: Boxer Christopher Rivera showcased his passion in life and death. After he died, he was propped up in a fake boxing ring in a community recreation center.

Treasure Hunt: An interesting way to pay tribute to someone’s life is to structure the funeral like a treasure hunt. Clues and maps can be given to loved ones taking them on a tour of meaningful locations for the deceased, including homes, favorite shops, restaurants or even wilderness spots. Mementos and memorials left in these locations may inspire participants to remember and share their own memories about the person.

Home Funeral: Those who value simplicity may opt for a home funeral, often combined with green funeral practices. At a home funeral, friends and loved ones can honor the deceased’s memory in the comfortable, familiar surroundings of his or her own home.

Social Media Funeral: Technology continues to connect us in new ways. From live-streaming the actual service to sharing memories in online memorials, we can now share important events with those who cannot be there in person. Digital services also make it easier to record memories to be shared and read at the convenience of family and friends.

Fireworks funeral: If the deceased is someone who would want to go out with a bang (literally), a number of companies will include a portion of cremated remains in custom-made fireworks, and then conduct a pyrotechnics display as part of a memorial service.

Holographic Eulogy: Holographic eulogies allow the dearly departed to attend their own funerals and speak about the people and things that mattered most to them in life. Some funeral homes offer this as part of their pre-need services and the recording can be made years in advance, when the person is in good health, the way they would most like to be remembered.

Burial Options

Here are some additional alternative options you may want to consider for your remains:

Burial Pods: Founded in Italy, the Capsula Mundi project involves organic burial pods that turn loved ones into trees. They are organic, biodegradable burial pods that literally turn a person’s remains into nutrients for a beautiful tree growing directly up above.

Biodegradable Urns: Poetree is a funeral urn that allows you to plant a tree with a loved one’s ashes, while also providing a simple but elegant monument. Relatives can place the deceased’s ashes in the urn and take it home, along with a boxwood tree sapling in a biodegradable pot. When ready, the cork stopper is removed, soil can be poured inside the urn, and the small tree may be planted in the ashes.

Whimsical Urns: Italian businessman Renato Bialetti chose to have his cremated remains interred in an urn fashioned to look like a Moka pot. The famous coffee pot was manufactured by his family’s company and he played an important role in popularizing it throughout the world.

Under a little house: At the intersection of Russian Orthodox religious tradition and Native Alaskan funeral rites, are the Burial Spirit Houses standing outside of St. Nicholas Orthodox Church in Eklutna, Alaska. According to tradition, when someone dies their body is buried and a blanket is placed over the grave. After the blanket has been there for a while, a little wooden house, about the size of large dollhouse, is placed over the grave, and is painted in the family colors. Unlike more traditional burial sites, the little houses are not kept up or restored, and are simply allowed to disintegrate back into the ground. In fact, this decay is part of the tradition.

On the side of a cliff: The people of the Sagada region of the Philippines aren’t afraid to show off their dead. In fact, they are known for their tradition of hanging exposed coffins from a cliffside. In a practice that dates back thousands of years, the Sagada carve their own coffins before they die (or a family member does it for them), and then they are hoisted up to literally hang around with their ancestors. Many of the hanging coffins are hundreds of years old, and they all have a unique look and feel since they were made by the person inside of them. It almost looks like a cross-section of a traditional in-ground cemetery.

In a modern art “cemetery”: Created as a proof of concept in 1972 by architect Aldo Rossi, the modern art “cemetery” takes the form of a big bright orange cube with a grid of square windows that would have been where the dead were buried. Unfortunately, Rossi himself died in 1976, and he was never able to see his super-efficient body box put to use. It won a number of design awards, but no body has yet to be buried there. Maybe you could be the first.

Make Your Burial Desires Known While You Still Can

What if you want your body or your ashes to be planted with seeds to grow a new tree, or if you want to be placed in a whimsical urn? How would your loved ones know if you haven’t indicated your wishes in your Advance Medical Directive?

Our proprietary 4-Needs Advance Medical Directive(TM) enables you to set forth your preferences with regard to organ donation, funeral arrangements, and disposition of remains. The document also accomplishes several essential things. In your 4-Needs Advance Medical Directive(TM), you can appoint an agent and give that person the power to consent to medical and health care decisions on your behalf. This person can decide whether to withhold or withdraw a specific medical treatment or course of treatment when you are incapable of making or communicating an informed decision yourself. Our 4-Needs Advance Medical Directive(TM) also contains a proprietary Long-Term Care Directive(TM) that allows you to address numerous issues that arise if and when long-term care is needed and you’re unable to communicate your wishes. You can also indicate your wishes concerning the use of artificial or extraordinary measures to prolong your life in the event of a terminal illness or injury.

If you have not done Incapacity Planning (including our 4-Needs Advance Medical Directive(TM) and Financial Power of Attorney), Estate Planning, or Long-Term Care Planning, or if you have a loved one who is nearing the need for long-term care or already receiving long-term care, please contact us to schedule your appointment for our no-cost initial consultation:

Fairfax Estate Planning: 703-691-1888

Fredericksburg Estate Planning: 540-479-1435

Rockville Estate Planning: 301-519-8041

DC Estate Planning: 202-587-2797

Critter Corner: Medicaid and Prepaid Funerals

{kind=link}

Dear Angel,

We are considering whether to prepay for my husband’s funeral to lock in prices, to relieve the burden of family members during what will surely be a stressful time, and to ensure his personal wishes are carried out. He is in the early stages of dementia and will need nursing home care in future. Will prepaying for his funeral affect Medicaid planning?

Thanks!

Peri Arranged

—-

Dear Peri,

A prepaid funeral contract is a legal agreement that allows a person to pay now for funeral services that will be needed sometime in the future. This contract may include the funeral or memorial service and other related services. A prepaid funeral contract may be revocable or irrevocable. Irrevocable means the contract cannot be canceled. Only a properly-established irrevocable funeral contract is an exempt asset for Medicaid purposes.

Medicaid does not pay for funerals, but it does have rules that allow you to set aside money for your own funeral, burial, or cremation without having that money “count” as part of your assets when Medicaid determines your eligibility for long-term care coverage. Qualified funding vehicles, such as funeral insurance policies and trust accounts are allowed, provided they are irrevocable and non-refundable, and cannot ever be used for purposes other than funeral expenses. When the proper funding vehicles are used to prepay a funeral, the value of the prearranged funeral contract and the funding vehicle are excluded as a countable resource in determining SSI & Medicaid eligibility.

You can read more about this topic in our Prepaid Funeral FAQs.

Hope this helps!

Angel

I’m Disabled, Not Incompetent…Why Can’t I Establish My Own Trust?

By Fredrick P. Niemann, Esq. of Hanlon Niemann & Wright, a Freehold, NJ Special Needs Attorney

Special Needs Trusts (SNTs) are an important tool in an elder care attorney’s toolbox. Established correctly, SNT’s allow a person to qualify for public benefits such as Medicaid and/or SSI while maintaining assets in a trust to supplement the funds provided by such programs. SNTs are established with funds that are owned by and belong to the beneficiary. By placing the assets into an SNT, the beneficiary can reduce his or her resource level to below the $2,000 threshold required by Medicaid and SSI to qualify for benefits. Unlike SNTs established with the funds of others (i.e., parents, grandparents, relatives, etc) a first-party SNT requires that a government payback provision be set forth in the trust.

Since 1993, it has been a legal requirement that a special needs trust be established by a parent, grandparent, guardian or court. This requirement has caused problems for many competent disabled adults who want to establish their own trusts. Certain other trusts which qualify as a form of a special needs trust that are run by non-profit third parties for beneficiaries allow beneficiaries to create their own trust. Because of this unfairness, the Special Needs Trust Fairness Act was filed with Congress in 2015 asking for a law allowing competent disabled adults to establish their own SNTs for themselves.

Currently, the act has passed the U.S. Senate and is now under consideration by Congress. As an issue of policy, it is likely the bill will pass the full Congress as well. Passing this bill will cut down on unnecessary costs for disabled adults. It will also offer us, as elder care attorneys, another option to protect clients who are receiving benefits. Imagine the convenience to the disabled that will be achieved by establishing their own trust, picking their own trustees and having funds readily available for the remainder of their lifetimes to supplement their SSI benefits without the necessity of court intervention.

To discuss your NJ Special Needs matter, please contact Fredrick P. Niemann, Esq. toll-free at (855) 376-5291 or email him at fniemann@hnlawfirm.com. Please ask us about our video conferencing consultations if you are unable to come to our office.

Our Top 10 Scariest Articles of 2016 (If You Dare)

{kind=link}

With Halloween upon us, now is the time when we present you with this year’s scariest stories. From one typo costing you your computer to loved ones with Alzheimer’s owning guns, we uncovered some scary ground. To celebrate Halloween, we’ve ranked our scariest articles from least to most scary (but you be the judge) for you to revisit, if you are brave enough to do so. As always, thank you for reading our newsletter and blog!

Note to our readers: if you’re someone who hates thinking about horrific topics, such as spending hundreds of thousands of dollars on long-term care, then you might want to stop reading or proceed with caution. But if you’re curious, please read on. . .

10. Veterans May Have a Higher Risk of Getting Alzheimer’s: Alzheimer’s researchers have become concerned that brain injuries, possibly even mild to moderate concussions, can cause brain inflammation that then triggers the development of Alzheimer’s in those who may already be at increased risk of the disease. It has also been found that Veterans who have experienced PTSD are twice as likely as those without PTSD to develop dementia.

9. Massive Amount of Romance Scams Target Older Victims: Millions of Americans visit online dating websites every year hoping to find a companion or even a soulmate. The FBI is warning seniors and others that criminals are using dating sites, such as Match.com, eHarmony, Plenty of Fish, and even social media sites such as Facebook, as well as direct email, to turn the lonely and vulnerable into fast money through a variety of scams. The FBI’s Internet Crime Complaint Center (IC3) reported aggregate losses to their victims at $204 million for 2015 alone. According to the IC3, romance scams were the largest personal fraud crime based on losses reported last year.

8. One Typo Could Cost You Your Computer: AARP reported that cybercrooks are using .om websites to spread computer malware, remotely access PCs and Macs, and to steal log-in credentials. Malicious criminals for years have been buying domain names with a missing or misplaced letter in website addresses belonging to well-known companies, and they simply wait for you to make a typo. Most of the .om-ending sites operate the same way: They don’t directly install malware but, instead, lead to other infected pages. Actors behind this “typosquatting” attack have been quite successful, as there are at least thousands of queries per day to the malicious .om domains from different computers across the world.

7. Huge Rate Hike for Federal Government Long-Term Care Insurance Policies: According to the Federal Long-Term Care Insurance Program (FLTCIP) Website, a new contract was recently awarded to John Hancock Life and Health Insurance Co., that will result in larger out-of-pocket costs for Federal Long-Term Care Insurance Program enrollees in the fall of 2016. The new, seven-year contract retains John Hancock, which last received the contract in 2009. Since the last contract, insurance rates increased annually for enrollees who opt not to pay higher costs up front, at a 4% to 5% annual inflationary increase. In 2009, FLTCIP enrollees saw their premiums jump by as much as 25%. Now, premiums are increasing by a whopping 225%! This is a previously unheard of increase for the FLTCIP program.

6. Do Not Resuscitate Orders Being Placed Without Patient Consent?: In England, hospitals are failing to tell relatives that they do not intend to attempt potentially lifesaving techniques to save their loved ones, according to the Royal College of Physicians. An audit of 9,000 dying patients found that one in five families were not informed of the plans – equivalent to 40,000 patients a year. In 16% of cases, the study found there was no record of a conversation with the patient about the order, and no planning documents were located. No matter where you live, ensuring that your wishes are met in these instances are more reason to have Advance Directives in place!

5. Caution: The Hidden Dangers of Heartburn Medicine: Currently, an estimated one in 14 Americans are dependent on an over-the-counter PPI to treat GERD (Gastroesophageal Reflux Disease). Considered the most effective treatment for GERD, PPIs are approved by the Food and Drug Administration (FDA) for use. The problem is that studies have linked long-term use of PPIs to an increased risk of dementia, cardiovascular disease, and renal failure, but until this year, scientists haven’t known exactly why. Results published in the journal Circulation Research earlier this year found that vascular cells chronically exposed to PPIs accelerate blood vessel aging— an effect that can have an adverse impact on cardiovascular health. This type of damage is synonymous with age-related chronic conditions and neurodegenerative disorders such as Alzheimer’s disease, cardiovascular disease, and cancer.

4. A Parent has Alzheimer’s and a Gun. What Do You Do?: Currently, around 40% of the country’s older population has a firearm in the home, according to the Pew Research Center, and about 11% of people 65 and older have Alzheimer’s. People with Alzheimer’s can become aggressive and hallucinate, sometimes lose peripheral vision, fail to recognize loved ones, and forget the purpose of an object. Therefore, a person who has Alzheimer’s or another form of dementia with a gun can make for dangerous, and sometimes deadly, consequences. Unfortunately, in most cases, families are not removing guns after a diagnosis. In one assessment, which examined 106 patients at a South Carolina clinic, 60% of them still had a firearm at home. In another, involving 495 people at a Cleveland clinic, 18% did. The Alzheimer’s Association offers guidance on how to minimize risks associated with firearms in homes where a loved one has dementia.

3. Must Read: Fluoride May Be Toxic for Seniors: Many of us experience loss of bone mass and density as we age. Of course, we want to do what we can to make our bones stronger, not weaker. However, if you are ingesting fluoridated water or anything with fluoride in it, you could be doing more damage to your bones than you know. According to a National Institute of Health (NIH) study, fluoride exposure alters the quality of bone tissue, and may increase the rate of bone fracture. According to the World Health Organization, excess fluoride intake causes a condition known as skeletal fluorosis, which has symptoms that are difficult to distinguish from arthritis in its early stages. In advanced skeletal fluorosis (also called crippling skeletal fluorosis), your extremities become weak and moving your joints becomes difficult, and your vertebrae partially fuse together, effectively crippling you.

2. $10,000 – $12,000? That’s for a Year, Right?: The cost of a nursing home in the metro DC area is $10,000- $12,000 A MONTH, an amount that is catastrophic for most of us. Each few years, Genworth conducts surveys of long-term care across the U.S. and summarizes the data in a Cost of Care Study, in an effort to help Americans plan for the potential cost based on their preferred location and setting. The 2016 survey is now out, and provides state-specific cost of care data for all 50 states and comparison to the national median. Unfortunately, according to the study’s findings, the cost of receiving care continues to rise sharply year over year, especially for services in the home, where most Americans prefer to receive long-term care.

1. If You Don’t Visit Your Parents, It Could Affect Your Credit Score: When you go to buy a car or refinance your mortgage, you of course try to take advantage of the best interest rate available. What if the sales person tells you that they are sorry, but your credit score is too low to do so? You are shocked because you pay all of your bills on time. Then, you find out that because you didn’t visit your mom and dad enough, your credit score was lowered. Sounds crazy, right? Well, as of May 1, 2016, this has become a reality for those living in Shanghai, China. That’s right! Under new rules, all citizens of working age who live apart from their mother and father must “visit or send greeting often,” or they will face a harsh penalty — the authorities could intervene to lower the neglectful children’s personal credit scores. There is probably little risk that any similar law would be enacted in the U.S. However, 29 states, including Virginia and Maryland, have filial responsibility laws making children financially responsible for the care of their indigent parents.

If you are now officially freaked out, and if you or a loved one has not done Long-Term Care Planning, Estate Planning, or Incapacity Planning (or had your Planning documents reviewed in the past several years), please call us to make an appointment for a no-cost consultation:

Fairfax Elder Law: 703-691-1888

Fredericksburg Elder Law: 540-479-1435

Rockville Elder Law: 301-519-8041

DC Elder Law: 202-587-2797

Making Sure Your Money Goes to the Right Place

{kind=link}

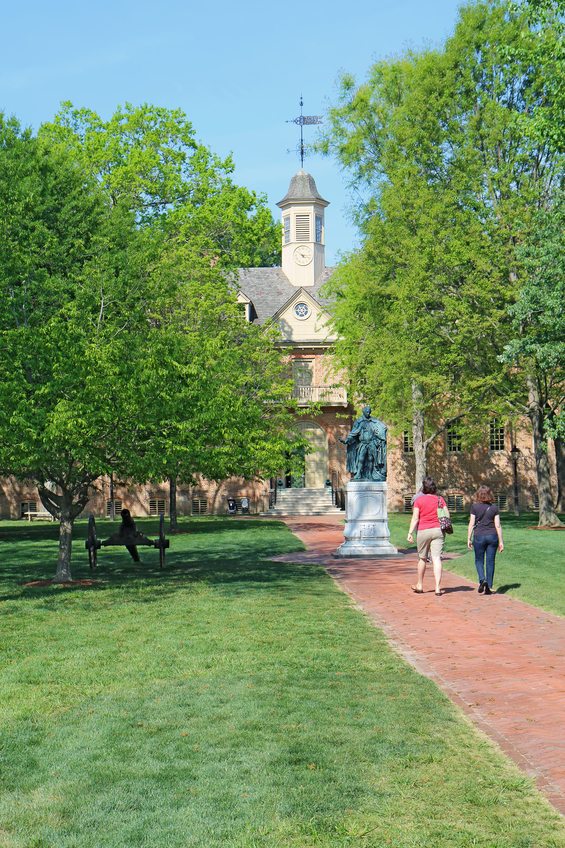

Q. When I read your bio, I noticed that you went to William & Mary for Law School. I went there for undergrad and for grad school, and love everything about the place, from the picturesque campus to Lake Matoaka in the Fall. I am a history buff with a PhD, who took full advantage of Colonial Williamsburg buildings and attractions, Jamestown Settlement, Historic Jamestown, and the Yorktown Settlement being so close by. I was so enamored with the place that I stayed an extra 20 years after graduating, and worked as a history professor at the university.

Now, I am retired and have moved to the DC area. I am widowed and my wife and I never had any children. I have lived a pretty simple life, and have saved quite a bit of money through the years. Although I am now in my early 70’s, I have never done estate planning, and think it’s about time I should!

When I do my planning, I know I would like to leave the bulk of my assets to my beloved alma mater, William & Mary. However, I recently read about Robert Morin, a man at the University of New Hampshire (UNH) with a similar desire and devotion to his college. He left $4 million dollars to UNH, and now the college is using $1 million of the amount to build a scoreboard for its stadium. It doesn’t seem like that is what he would have wanted, having read about him, and it seems his Will had to go through a timely and expensive probate process before the university even saw any of the money. Is there a way to avoid a similar fate from happening to my bequest? Since I am single, is a Will all the planning that I need? Thanks for your help!

—

A. Thank you for your inquiry. It is always nice to hear from and to meet fellow William & Mary alumni!

The man you mentioned, Robert Morin, a University of New Hampshire (UNH) graduate, worked for nearly 50 years at his alma mater’s library and saved a fortune of money, due to his frugal lifestyle. According to a recent Boston Globe article, Morin rarely bought clothes, drove a 1992 Plymouth, and spent most of his spare time reading, keeping to himself, and working at the university library.

Morin, who died a little over a year ago, left his alma mater his entire estate of $4 million (a nest egg that few people knew he had), but didn’t leave instructions on exactly where he would like the money to be allocated. After the bequest cleared probate court, the university announced that it will use $1 million of the money for a new video scoreboard at the football stadium.

Critics allege that using Morin’s gift for a scoreboard is inappropriate, given his bookish life, and that the money would be more appropriately used for scholarships, books, computers, research grants, etc. One UNH alumnus blogged: “As a Wildcat, I feel deeply saddened and honestly completely ashamed of my alma mater for this.” Of course, we will never know what Morin would have to say about all this. Anecdotally, however, if it was so important to him to designate exactly where he wanted the funds to go, he could have been more specific in his estate planning documents.

Avoiding the Nightmare of Probate

The part of the situation that certainly could have been avoided was Morin’s estate going through probate. The situation for many people is that when they think of Estate Planning, they immediately think of preparing a Last Will and Testament. While having a Will is slightly better than dying without a Will (i.e., dying intestate), Wills create the same major problem as dying intestate – this being that a Will forces your estate to go through the nightmare of probate, as Morin’s did.

The probate process is a “nightmare” because it includes proving the authenticity of a person’s Will, appointing an executor, identifying and inventorying every penny of a person’s assets, paying debts and taxes, identifying heirs, and eventually, sometimes years later, distributing property according to the Will, or if no Will is available, according to state law. These are five detailed reasons why probate is such a headache:

1. Probate requires frustrating intrusion by the court, lawyers, and the public into a very emotional, private, family time. A judge or commissioner may have to determine who is a legitimate creditor, and may have to rule on distributions to children and other beneficiaries. Your estate will likely have to hire a lawyer to guide the executor through the legal maze.

2. Probate is public: A Will gets filed in the courthouse, for all to read. And Wills are read. They are read by salesmen, by newspaper reporters, by the morbidly curious, and by scammers and con artists all seeking in one way or another to take advantage of the publicity required by the probate process.

3. Probate is timely: Unless your executor is absolutely certain that there are no debts owed by the estate (a rare occurrence, since almost everyone leaves some small debts behind) and is willing to accept personal responsibility for your debts, the Virginia probate law mandates that your assets not be distributed for one year after you die, to allow creditors time to petition the court for full payment. Any assets distributed before that time come with a heavy cost for your executor — he or she is personally liable for the repayment of all of this amount, even if the beneficiaries to whom distribution is made have already spent the amount distributed. Thus, your executor will likely be very hesitant to distribute before all debts and taxes are paid. The court, not your family, will supervise and authorize the settling of all debts and the payment of inheritances, in its time and with its delays.

4. Probate is costly: On a national average the probate process takes from five to eight percent of your family estate out of the hands of your beneficiaries and gives it to the courts and other outside individuals. Planning with a trust can save the average American family about $30,000 in probate fees, attorney fees, and court costs alone, according to a national study by the AARP. The upfront cost of a trust is only slightly higher than just a will, but the savings in the end always makes the initial expense more than worthwhile.

5. Potential guardianship and conservatorship proceedings can be avoided: If you are not competent at any time before your death, the trustee of your living trust can serve as the caretaker of your property. This can avoid the expensive and embarrassing public process of a guardianship and conservatorship proceeding, where your children have to prove that you are not able to manage your own affairs. A living trust combined with a power of attorney provides the most complete protection available.

Using a Revocable Living Trust (RLT)

With a Revocable Living Trust (RLT), you can provide how the real estate and other trust property is to be distributed at your death. As with a Will, you can provide for any number of special situations. However, at your death, the trust assets may be quickly distributed according to the terms of the trust, without the delay, fees, and public exposure of probate.

An RLT does not eliminate the need for a Will. A “pour-over Will” is still necessary to pass on those assets you did not transfer to the trust prior to your death. Please read more about Revocable Living Trusts as a vehicle for estate planning here.

Yes, You Should Still Plan for Yourself if You Are Single

Sometimes, it’s almost more important for single people to do estate planning. One reason is that when a married person suffers a major illness, it’s usually pretty clear who will take on medical and financial responsibility. For unmarried individuals, the water could be a bit murkier.

In addition, when it comes to your finances, if you are unable to pay your bills and take care of your other legal and financial affairs for a period of time, who do you think will do so? The answer to that is: whomever the courts say. And first off, someone will have to go to court and have you declared legally incompetent, even if it is only for a temporary period of time.

Finally, what will become of your things if you should unexpectedly pass away? Who would have legal rights to your belongings, to your home, to your pets? Without clearly outlining your wishes with an estate planning attorney, you have very little control over the matter. In your situation, you need to make what’s called a “restricted gift” to our mutual alma mater. A restricted gift is one that can be used only for a specific purpose, in a specific geographic area, or within a specific time frame. For example, a donor can place restrictions that require the gift to be used for a specific program and to not be used for overhead expenses. When an organization accepts a restricted gift, it accepts the donor’s restrictions and must honor those restrictions.

Incapacity Planning Documents that all adults should have in place include an Advance Medical Directive, a Financial Power of Attorney, and a Lifestyle Care Plan. Estate Planning Documents that most people should have include a Revocable Living Trust & Pour-Over Will. These are crucial in ensuring that your wishes are met and that you have control over your future. An experienced estate planning attorney such as myself can easily get you on the path to having these affairs in order. Call us to set up an appointment for a no-cost consultation:

Fairfax Estate Planning Attorney: 703-691-1888

Fredericksburg Estate Planning Attorney: 540-479-1435

Rockville Estate Planning Attorney: 301-519-8041

DC Estate Planning Attorney: 202-587-2797

Can I have a New York Notary Notarize a Document for Me in New Jersey?

By Fredrick P. Niemann, Esq. of Hanlon Niemann & Wright, a Freehold, NJ Elder Care Attorney

Recently, a client, who lives in New York, was seeking to have a power of attorney document notarized in New York even though his mother, whom he was assuming power of attorney over, lived in New Jersey. While it is possible for notarized documents to be recognized out of state as being notarized, a notary’s jurisdiction is bound to the state of physical witness and presence. This is codified in New York Executive Law, which states that “notaries in this state shall have a jurisdiction that is co-extensive with the boundaries of the state.” The power of attorney was prepared in New Jersey for a resident living in New Jersey. The document should therefore be notarized by someone who has the jurisdiction to notarize New Jersey documents, which New York notaries do not have. Therefore, the New York notary cannot legally notarize her document.

Interestingly, other states have different laws when it comes to notaries. Kentucky, for example, allows notaries to apply for a special commission to notarize documents outside of the state as long as they are recorded in Kentucky. Notaries in Montana, North Dakota, and Wyoming have the ability to notarize documents in each other’s states. In Washington D.C. and Virginia, any resident or person who is employed in the state but lives somewhere else may apply to become a notary public. Check out the laws where you live to see how notarization works for you and how your state recognizes notaries.

To discuss your NJ Elder Care matter, please contact Fredrick P. Niemann, Esq. toll-free at (855) 376-5291 or email him at fniemann@hnlawfirm.com. Please ask us about our video conferencing consultations if you are unable to come to our office.

7 Reasons You Don’t Want To Be A Hero In Caregiving

{kind=link}

Guest Post By Jennifer Fitzpatrick

“She heroically cared for her mother.”

“He is a real hero in the way he’s caring for his wife.”

I’ve heard many versions of this sentiment referring to someone in the caregiving role as a “hero.” While the person commenting means to give the caregiver a compliment, the term “hero” can unintentionally pressure mere mortal caregivers to be superheroes. Here are 7 reasons why caregivers should not strive to be heroes:

1. Heroes are super-human. Caregivers are not. Caregivers are simply human beings doing their best to take care of someone they love who is injured, ill or disabled. They don’t possess the super powers or mystical abilities of a superhero. Caregivers sometimes wish they did have super powers but it’s important for those of us who support them to acknowledge that they don’t have a magic wand to fix all of their loved one’s problems.

2. Heroes tend to have no social life. The Fox Television show ‘Gotham’ depicts a teenage Bruce Wayne training for his future as Batman rather than playing sports, video games or just hanging out with friends.

While heroes like Bruce Wayne don’t socialize much, caregivers who want to be physically and mentally healthy should. Socializing, taking breaks and not isolating themselves are essential for a caregiver to remain as healthy as possible so he or she can maintain the caregiving role.

3. Being a hero is tough on romantic relationships. Consider Spiderman/Peter Parker’s ongoing challenges with Mary Jane. Superheroes are constantly making big sacrifices for the “greater good” so their personal relationships suffer.

Caregivers should not sacrifice their romantic relationships when taking care of a loved one. When a marriage or romantic relationship suffers, caregivers have less emotional support. No matter how busy caregivers are with the loved one they care for, they should always prioritize their partners too.

4. Heroes are secretive and lonely. Heroes can’t be themselves all the time. Most superheroes are dressing up in costumes and hiding their true identities. Very few people know the real person behind the hero façade.

Caregivers whose costume includes acting like they always have everything together are typically falling apart behind closed doors.

5. Heroes don’t always collaborate well. Heroes often have difficulty admitting when they need help. For example, Superman tends to carry the weight of the world on his shoulders.

While many caregivers struggle with asking for and accepting help, especially initially, it is absolutely essential for the caregiver’s well-being. No caregiver should exist in a vacuum. The primary caregiver needs to be the captain of the ship with plenty of first mates.

6. Heroes are invulnerable. The DC Comics’ website cites invulnerability as a superpower possessed by both Wonder Woman and Superman.

I have never met a caregiver who wasn’t vulnerable. Caregivers give their money, energy and time to care for a loved one, often expecting nothing or very little in return. They are frequently criticized by others in the family for “not doing it right.” They are also quite vulnerable to physical and mental health conditions when they don’t get help with their caregiving duties.

7. Heroes have unrealistic expectations of themselves. Recently when watching Christopher Nolan’s Batman film series, this was illustrated when Michael Caine’s Alfred reminds Bruce Wayne to know his limits. Christian Bale responds that Batman has no limits.

Caregivers who believe they have no limits and hold unrealistic expectations of themselves are headed for burnout. Who will care for the loved ones dependent on them when the caregiver crashes and burns?

Aim to be a real-life, human, good enough caregiver. Maintain relationships. Socialize. Have realistic expectations of yourself. And most importantly ask for help. Stop trying to be a hero—it’s impossible and unnecessary.

Jennifer L. FitzPatrick, MSW, LCSW-C, CSP (Certified Speaking Professional), a gerontology instructor at Johns Hopkins University is the author of Cruising Through Caregiving: Reducing The Stress of Caring For Your Loved One (www.cruisingthrough caregiving.com) which was published on Sept. 27, 2016. The founder of Jenerations Health, she helps organizations and individuals boost productivity, morale and revenue through generational awareness. You can find her at www.jenniferfitzpatrick or on twitter @fitzpatrickjen.

New Virginia Regulations Limit Caregiver Pay

{kind=link}

Stephen Grammer suffers from cerebral palsy, a physical disability that makes it impossible for the 36-year-old to walk, feed himself, or go to the bathroom on his own. Currently, he’s able to live alone in an apartment because he has caregivers with him 16 hours a day. However, Grammer worries that his independence is in jeopardy because of a recent law passed by the Virginia General Assembly that prohibits many caregivers for disabled Virginians from being paid overtime.

Due to low wages and lack of benefits, and now no overtime pay, thousands of personal care assistants in Virginia have less of an incentive to remain in difficult, low-paying jobs. Grammer explains that it’s “already a challenge to find qualified caregivers who are notoriously underpaid and the promise of no overtime makes it even harder to recruit and retain them.”

Federal Law Mandated Overtime Pay for Caregivers — What Happened in Virginia?

Last year, the federal Department of Labor extended the overtime and minimum-wage protections of the Fair Labor Standards Act to most home care workers, including the homecare workers paid by the state using tax-funded Medicaid dollars. In Virginia, Medicaid caregivers used to be paid “straight time” — their standard hourly wage — for any hours they worked beyond 40 each week.

After court battles, the Department of Labor rule went into effect in January 2016, and for the first time, the Commonwealth of Virginia had to start paying time-and-a-half for overtime. Between January 1, and June 30, 2016, Medicaid caregivers worked 2.1 million hours of overtime, according to a presentation given to the Virginia Disability Commission last month. Those hours cost the state an additional $11.2 million compared with the way caregivers had previously been paid. The state paid $407.4 million for 38 million caretaker hours worked in the full fiscal year that ended June 30. That year, 35,231 caregivers helped 21,231 people with disabilities, according to the Department of Medical Assistance Services, which administers Medicaid in Virginia. Despite the data on the number of people being helped, the Virginia General Assembly capped hours at 40 as of July 1, 2016.

Advocating for Change

Grammer is a 2013 graduate of the Partners in Policymaking program through the Virginia Board for People with Disabilities. He and other advocates have been trying to get the General Assembly to allow Medicaid-paid caregivers to work overtime — or at least allow exceptions in particular cases.

Governor Terry McAuliffe agrees that there should be overtime pay for caregivers of those with disabilities. In fact, his proposed budget for this fiscal year included funds to pay for up to 56 hours of labor a week for home care workers, said Joe Flores, Virginia’s deputy secretary of health and human resources. That would have covered 40 hours of straight time and 16 hours of time-and-a-half overtime.

According to McAuliffe, the “elimination of all overtime for consumer-directed attendants could have a significant adverse impact on the continuity of care received by some of Virginia’s most vulnerable citizens and jeopardize the health of older adults and people with disabilities.” Despite the governor’s recommendations, the General Assembly failed to approve his change to the budget.

In Grammer’s case, his caretakers said they have been working for free because they don’t want to leave him alone.

Currently, Washington state, California, Florida and Massachusetts are among states that pay personal caregivers overtime, according to the National Employment Law Project. Vermont has created a process for requesting an exception to the overtime cap when a person with disabilities is at risk of harm or institutionalization.

Other Living Options for Adults with Special Needs

Most adults with special needs have a strong desire to live in their own homes and communities. Unfortunately, due to the shortage of home health aides due to overtime pay being cut and other issues, this may no longer be a viable option.

Here are some other housing options for adults with special needs:

•Family members. According to Care.com, 76% of individuals with developmental disabilities live at home. In a quarter of these situations, the average age of the adult child was 38; caregivers were age 60 or older.

•Community-based homes and supported living arrangements. Adults living in group homes enjoy some independence, but receive support as necessary depending on their needs. Caregivers living or working at these homes provide a range of services, from supervision to help with medication to advice on getting to work and dressing appropriately.

•Long-term care facilities. Some adult children with special needs require extensive support around the clock. In cases such as this, parents may feel their child’s needs are best served in a long-term, live-in care facility (i.e., a nursin home) which could be extremely costly ($10,000 – $14,000 a month in the DC Metro area). If this is the best option for your loved one, we can help you plan now for the catastrophic costs of long-term care.

Do You Have an Adult Child with Special Needs?

If you have a special needs child who will likely need care for life, it’s important to provide legal protections for your child. A special needs trust is recommended to protect a disabled individual’s financial future. Also known as Supplemental Needs Trusts, this type of trust preserves legal eligibility for federal and state benefits by keeping assets out of the disabled person’s name while still allowing those assets to be used to benefit the person with special needs. Read more here.

This month is National Special Needs Law Month. When it comes to special needs planning, The Law Firm of Evan H. Farr, P.C. can guide you through this process. If you have a loved one with special needs, call one of our offices to make an appointment for a no-cost consultation:

Fairfax Special Needs Attorney: 703-691-1888

Fredericksburg Special Needs Attorney: 540-479-1435

Rockville Special Needs Attorney: 301-519-8041

DC Special Needs Attorney: 202-587-2797

Understanding the Risk When You Place Your Child on Your Joint Bank Account

By Fredrick P. Niemann, Esq. of Hanlon Niemann & Wright, a Freehold, NJ Elder Law Attorney

Sometimes one of the biggest mistakes our clients make when they set up a bank account(s) is that they make the account a joint account with their son or daughter. They do this because they are worried that something might happen to them, and in the case of an emergency, his or her child will have access to the money to pay their bills and to take care of them. This type of joint account is often called a “convenience account”. While this may be a good idea for many families, it can have particularly dangerous consequences for your financial welfare and estate plan in the future. The reason for this is found a New Jersey law called the Multiple Party Deposit Account Act, which I discussed in an earlier blog. If multiple parties have their names on the account, N.J.S.A. §17:16I-5 requires that the account be treated as a joint account. This means that anyone who is named on the bank account and survives you becomes the owner of the money left in the account. The money does not go to your estate. So if you planned on giving your estate to all of your children equally, the end result will be that only the child whose name is on the bank account with you will get the money in the account.

Fortunately, if this mistake occurs and you die before correcting it, the law has a limited way to remedy the situation. But it often involves litigation. The Act says that if there is clear and convincing evidence that you did not intend a joint account it will be treated as a convenience account. It is often a tough case to prove, particularly when you die and cannot tell the judge your intentions, but there are two ways to show you did not intend to give the child the money solely. The first way to do this is to demonstrate that the child created a confidential relationship with you whereby they took care of your finances for you. So for example, if your child was/is handling all your finances, including driving you to and from the bank and executing checks on your behalf, it can be said that a confidential relationship was formed between you and your child such that you were influenced to jointly add your child’s name to the bank account.

But the other way to go about showing you did not intend to make your child the sole owner of the money in the account goes back to the purpose of why you created a convenience account. The courts understand that often a loved one is placed on the account of another for the purpose of handling the loved one’s financial affairs in the event of incapacity and/or poor health. But to win you must prove it and the standard to prove it is high. Without that proof, a court is likely to say that the money belongs to whoever is the joint account holder. In one case I recently read on the matter, Sadofski v. Williams, 60 N.J. 385 (1972), the daughter testified that the mother put her on her bank accounts in case something were to happen to the mother. The mother handled her own finances without participation from the daughter until the mother went to the hospital, where the daughter then testified that the mother instructed the daughter to withdraw the remainder of the money out of the account herself, as it was her money. The Court concluded that the daughter’s testimony that she was put on there as a fail-safe should something happen, along with the mother handling her own finances, meant the daughter was only on there for convenience purposes and the money therefore did not belong to her solely, but rather the estate of the mother.

The controversies around joint accounts can be avoided if you put in writing that you wish to have your child on your account solely for emergency purposes. If you are considering doing this, make sure you communicate this intention with the bank, and ask for a form that everybody can sign off on stating this is your intention. The Supreme Court in Sadofski chastised the bank for not doing this, noting how banks do not fully comprehend the law regarding joint accounts and the significance of placing other people’s names on the account. You now understand the significance of doing this.

To discuss your NJ Estate Planning, Estate Litigation and Elder Financial Abuse matter, please contact Fredrick P. Niemann, Esq. toll-free at (855) 376-5291 or email him at fniemann@hnlawfirm.com. Please ask us about our video conferencing consultations if you are unable to come to our office.

What is the Difference Between Alzheimer’s and Dementia?

{kind=link}

Recently, Gina’s mother told her the devastating news that her Uncle Jack had been diagnosed with dementia. When Gina’s husband got home from work, she quickly told him about her uncle’s “Alzheimer’s” diagnosis. Gina, her mother, and her husband began using the terms “dementia” and “Alzheimer’s” interchangeably, as if they meant the same thing, where in reality they do not. And, in the case of Jack, he actually was diagnosed with vascular dementia, which is quite different than Alzheimer’s disease.

Dementia and Alzheimer’s disease may share many of the same symptoms, but the two are not different names for the same condition. Alzheimer’s is actually one of the four most prevalent forms of dementia. Here’s what you need to know about the main forms of dementia (including Alzheimer’s) in order for you to avoid this common mistake:

Dementia

The term “dementia” is used to describe a set of symptoms that can include memory loss, difficulty thinking, problem solving, or issues with language. Dementia is caused by damage to the brain cells. Because Alzheimer’s is a disease that destroys the brain, it is one of the most common forms of dementia.

These are the other most prevalent types of dementia:

Vascular Dementia

● It is also known as “multi-infarct dementia” or “post-stroke dementia.”

● It is the second most common type of dementia.

● Main symptoms often include memory loss, impaired judgment, a decreased ability to plan, and loss of motivation.

● The cause is often bleeding within the brain from a stroke or multiple mini strokes (TIAs) that cause brain damage.

● Vascular dementia cannot be cured, but people who have the ailment are treated to prevent further brain injury from the underlying cause of the ailment. Numerous medication and therapies may be used to help manage the symptoms.

Lewy Body Dementia

● It is also known as “cortical Lewy body disease” or “diffuse Lewy body disease.”

● It is the third most common type of dementia.

● Main symptoms often include sleep problems, memory loss, hallucinations, and frequent swings in alertness.

● The cause is Lewy bodies –abnormal proteins that appear in nerve cells and impair functioning.

● There is no known treatment to reverse Lewy body dementia or address its underlying cellular cause but, as with other the other main types of dementia, a wide array of therapies and treatment are used to improve the patient’s quality of life and alleviate symptoms.

Frontotemporal Dementia

● It is fairly rare, but believed to be the fourth most common type of dementia.

● Frontotemporal dementia is marked more by behavioral and emotional changes than by cognitive impairment. In fact, memory is preserved in people with frontotemporal dementia.

● Main symptoms often include decreased inhibition (frequently leading to inappropriate behavior, apathy and loss of motivation, decreased empathy, repetitive or compulsive behaviors, and anxiety and depression.

● Frontotemporal dementia occurs when the frontal or temporal lobes of the brain are damaged or shrink.

● Frontotemporal dementia cannot be cured or reversed, but doctors will use medicines to treat uncomfortable or problematic symptoms.

Other Causes of Dementia

Just about any condition that causes damage to the brain or nerve cells can cause dementia. For example, people with Parkinson’s disease will often exhibit dementia in the later stages of their illness. Huntington’s disease, Creutzfeldt-Jacob disease, and alcoholism can all lead to irreversible cognitive impairment / dementia.

Alzheimer’s Disease

As explained, Alzheimer’s is just one form of dementia –the most common one, with as many as 50 to 70% of all dementia cases being caused by Alzheimer’s.

According to the Alzheimer’s Association, Alzheimer’s Disease is caused when high levels of certain proteins inside and outside brain cells make it hard for brain cells to stay healthy and to communicate with each other. This leads to the loss of connections between nerve cells, and eventually to the death of nerve cells and loss of brain tissue.

Those with Alzheimer’s often experience memory loss that continues to get worse as the disease progresses, confusion, difficulty communicating, anxiety , and paranoia.

There are currently both pharmaceutical and non-pharmaceutical therapies which can temporarily increase functioning and improve the spirits of the person with Alzheimer’s disease, but no treatment has proven to be effective. The Alzheimer’s Association says, “At this time there is no treatment to cure, delay or stop the progression of Alzheimer’s disease.” However, the U.S. government has made Alzheimer’s research a high priority and set the optimistic goal of finding a cure by 2025. Vigorous research continues and numerous possible treatments are being investigated.

Think you or a loved one have Alzheimer’s or another form of dementia?

Doctors can accurately diagnose Alzheimer’s or symptoms of one of the other forms of dementia in 90% of cases. If you know someone who appears to be losing mental abilities to a degree that interferes with daily activities and social interactions, consult a doctor right away. As you can see from the details above, there are some medications and treatments that may help manage some of the symptoms, so it’s important to seek help as soon as possible.

Persons with Alzheimer’s disease and their families face special legal and financial needs. Controlling the high costs of caring for a loved one with Alzheimer’s, and navigating the emotionally and physically demanding requirements of caregiving, require the assistance of a highly skilled and specialized expert in the field of Alzheimer’s Planning.

At The Law Firm of Evan H. Farr, P.C., we are dedicated to easing the financial and emotional burden on those suffering from dementia and their loved ones. We help protect the family’s hard-earned assets while maintaining your loved one’s comfort, dignity, and quality of life by ensuring eligibility for critical government benefits such as Medicaid and Veterans Aid and Attendance. Please call us as soon as possible to make an appointment for a no-cost consultation:

Fairfax Alzheimer’s Planning: 703-691-1888

Fredericksburg Alzheimer’s Planning: 540-479-1435

Rockville Alzheimer’s Planning: 301-519-8041

DC Alzheimer’s Planning: 202-587-2797